SPY Financial Telemetry Report

Week Ending 2026-06-26

Published 2026-06-28

Market-State Telemetry from Options-Derived Expectations and Innovation Dispersion

The Vyreon Financial Telemetry Report summarizes current conditions using a multi-horizon expectation framework, innovation-based volatility diagnostics, and calibration monitoring. The objective is not to predict exact future prices, but to quantify how expectations, uncertainty, and structural conditions are evolving through time.

Executive Synthesis

Volatility continues to compress, and current price movement is characterized by lower model error relative to its recent smoothed trend. Near-term conditions remain mildly defensive with limited directional evolution, so the closest forecast window reflects a cautious but not disorderly environment. Long-term structure remains constructive, but it has softened from the prior snapshot. Medium-term structure remains negative but is recovering, leaving intermediate horizons unresolved rather than broadly confirming one directional story. Agreement across timeframes remains incomplete, and confirmation across timeframes remains unclear.

- Regime: Compressing volatility

- Near-Term (~2 to 4 weeks): Mildly defensive

- Short-Term (~1 to 2 months): Defensive and unresolved

- Medium-Term (~2 to 4 months): Recovering but still negative

- Long-Term (~6 to 12 months): Constructive but softening

- Structure: Fragmented

Market State

- Volatility is compressing, and realized behavior is fitting prior expectation structure more closely, which supports calmer movement but does not resolve directional uncertainty.

- Near-term structure remains mildly defensive with tight uncertainty, so immediate price behavior is more constrained but still lacks clear positive confirmation.

- Short-term structure remains defensive and stable or unclear, which keeps the one-to-two-month window sensitive to timing and failed continuation.

- Medium-term structure remains negative but is recovering, so intermediate behavior reflects improvement without enough adjacent confirmation to establish a completed transition.

- Long-term structure remains positive but is softening, which preserves a constructive longer-horizon reference while reducing the strength of that anchor.

- Cross-horizon consistency remains fragmented because the forecast horizons are not telling one consistent story, which limits confidence in broad directional interpretation.

- Cross-horizon confirmation remains unclear because medium-term improvement lacks support from adjacent horizons and is opposed by long-term softening.

Market Insights

- Price movement is becoming calmer as volatility compresses, which reduces variability-driven disruption and improves holding-period survivability for strategies that depend on orderly behavior because realized movement is diverging less from prior expectation structure.

- Near-term defensive behavior with tight uncertainty creates a narrow execution environment, which raises timing sensitivity for short-horizon strategies because the closest forecast window remains negative without meaningful directional evolution.

- Medium-term recovery reduces one-sided defensive pressure but leaves signal reliability incomplete, which makes larger directional commitments more timing-sensitive because adjacent horizons do not confirm the improvement.

- Long-term constructive structure is still present but has softened, which weakens longer-horizon conviction and places more weight on monitoring persistence because distant forward structure is moving against the medium-term improvement.

- The options surface is layered across near, medium, and longer expiries, which supports segmented interpretation rather than a single market-wide read because open interest is concentrated across multiple maturity groups.

What Changed This Week

- Near-term expected return moved lower, and the uncertainty band narrowed.

- Short-term expected return moved lower, and the uncertainty band narrowed.

- Medium-term expected return improved, and the uncertainty band narrowed.

- Long-term expected return softened, and the uncertainty band widened.

- The combined change profile shows compression in the closer and intermediate horizons, with wider long-term uncertainty and incomplete agreement across timeframes.

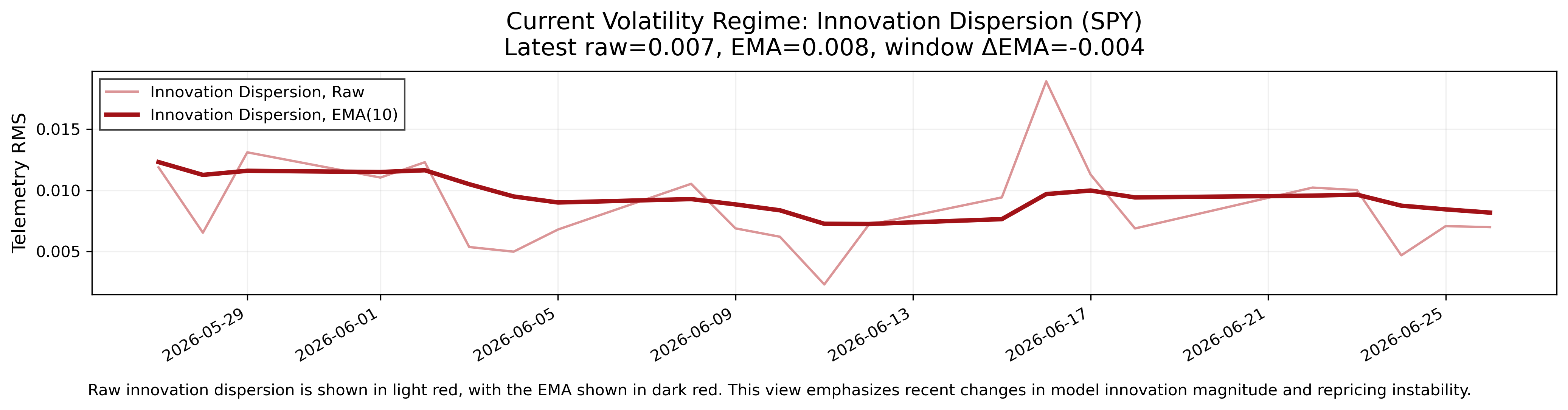

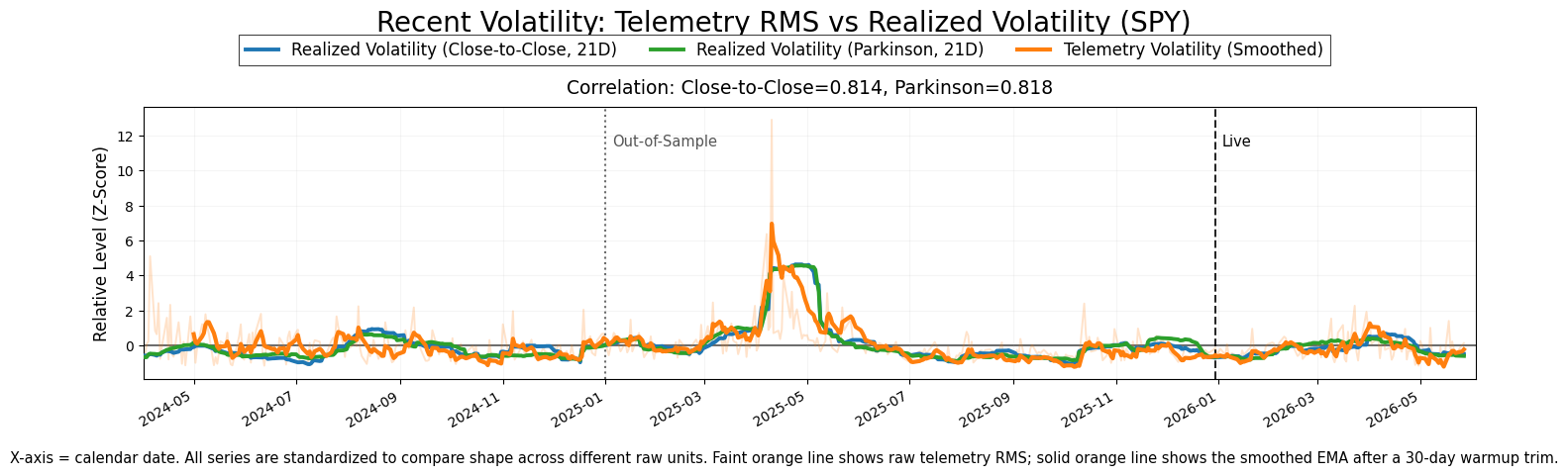

Volatility Regime

Volatility is currently compressing. Raw model error is below the smoothed volatility trend, and the smoothed trend has declined over the recent window. This reflects a market environment where realized behavior is diverging less from prior expectation structure.

In this framework, volatility is measured through the residual between realized behavior and the model's prior state estimate. Lower residual pressure means the market is requiring less frequent adjustment from the estimator. That condition is associated with more orderly movement, but it does not by itself create directional agreement across forecast horizons.

The current volatility state is therefore best read as declining instability rather than a resolved directional regime. Movement is less reactive than during higher-error conditions, but horizon-level structure remains mixed, with near-term defense, medium-term recovery, and long-term softening all present at the same time.

The following chart shows recent market volatility using the RMS of model error. The light line shows raw model error, while the darker line shows the smoothed trend. This view highlights short-term changes in variability and how current movement compares to its underlying trend.

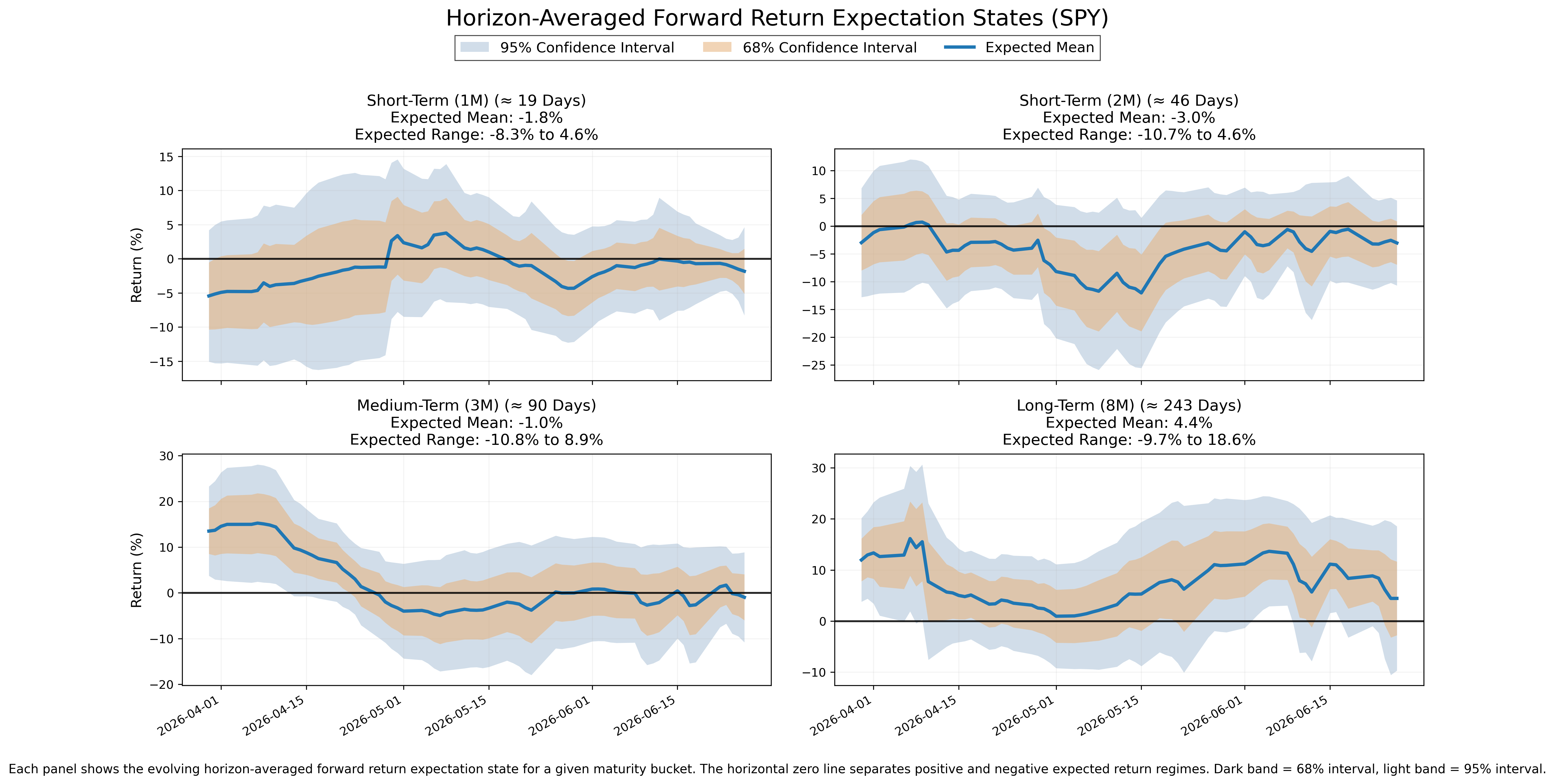

Horizon-Averaged Forward Expectations

Near-Term (~2–4 weeks)

• State: Mixed

• Uncertainty: Tight

• Interpretation: Near-term structure is mildly defensive and stable or unclear, with compressing volatility supporting calmer movement but tight uncertainty limiting the room for interpretation.

Short-Term (~1–2 months)

• State: Mixed

• Uncertainty: Moderate

• Interpretation: Short-term structure remains defensive without meaningful directional evolution, so movement in this window is unresolved and timing-sensitive.

Medium-Term (~2–4 months)

• State: Mixed

• Uncertainty: Moderate

• Interpretation: Medium-term structure remains negative but is recovering, with weak positive evolution showing improvement that still lacks broader confirmation across nearby horizons.

Long-Term (~6–12 months)

• State: Mixed

• Uncertainty: Wide

• Interpretation: Long-term structure remains constructive but is softening, so the distant forward view still has a positive center but weaker reliability due to wide uncertainty and negative evolution.

The following chart shows the evolution of horizon-averaged forward expectation states. Each panel represents a maturity window, with the central line showing the average expected return structure across that horizon bucket and shaded regions showing uncertainty.

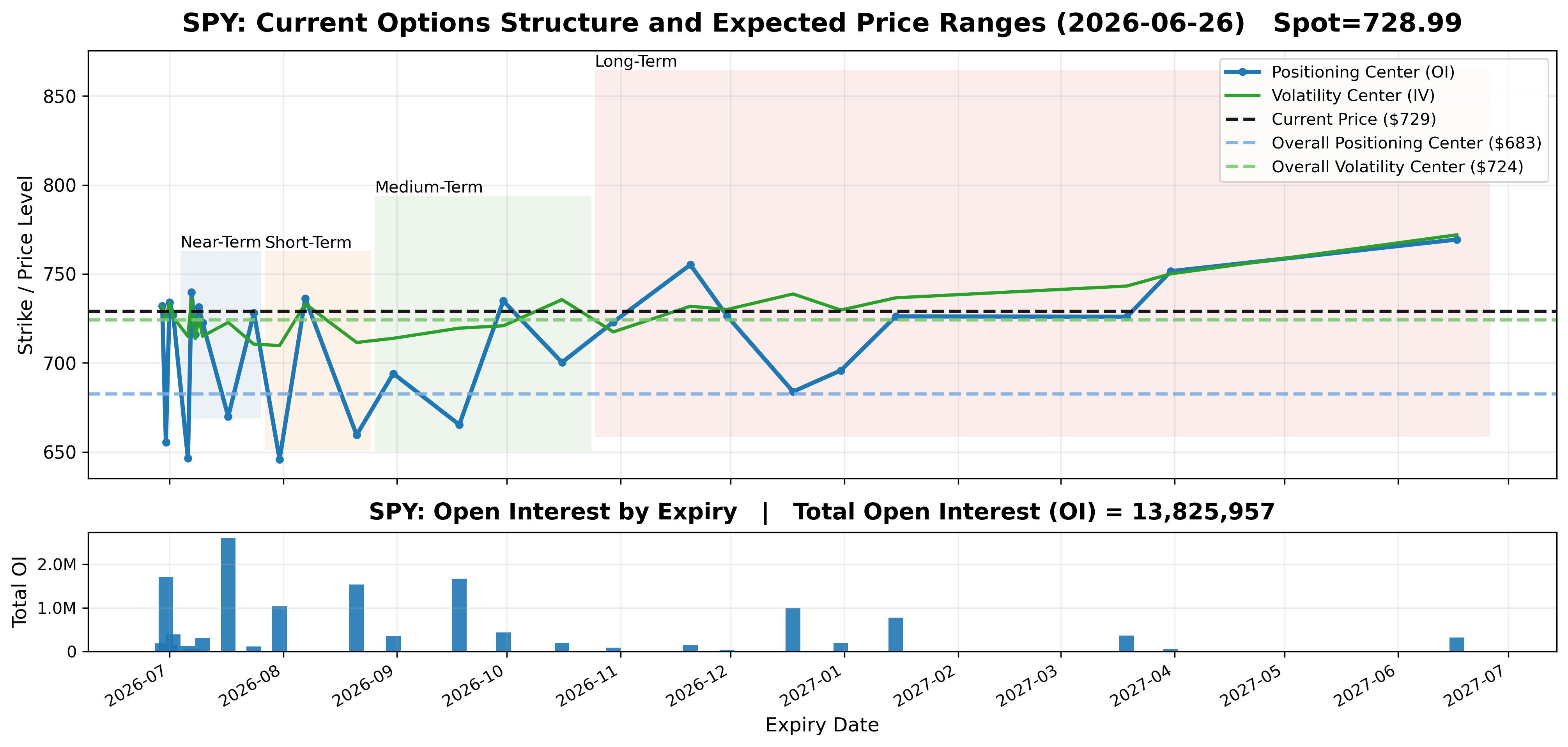

Options Market Structure

The options surface is organized across several maturity layers rather than being concentrated in only one expiration window. The largest listed open-interest concentration is the July 17 expiry, followed by June 30, September 18, August 21, and July 31. This creates a structure with meaningful near-term, short-term, and medium-term open-interest layers.

The listed expiries also show longer-dated participation through December 18, January 15, and March 19. This distribution indicates that open interest is not confined to the front of the chain. It is spread across multiple maturity groups, which is consistent with a segmented surface rather than a single concentrated expiration profile.

Spot is close to the overall volatility center and sits above the overall positioning center. This separation describes the current organization of positioning and implied-volatility structure. It should be treated as a cross-sectional surface condition, not as a directional signal or price target.

The following chart shows today’s options market structure across expiration dates. Each point represents a future expiry, with positioning (open interest) and volatility (implied volatility) centers derived from current options data. Shaded regions show the expected price ranges for each horizon based on current market conditions. This is a cross-sectional view at a single point in time, not a time-series.

Bottom Line

The dominant market condition is compressing volatility. Realized behavior is diverging less from prior expectation structure, which means the market is currently less unstable than the recent volatility trend. Near-term structure remains mildly defensive. Long-term structure remains constructive but has softened. Cross-horizon consistency remains fragmented, so the report does not describe a completed directional regime.

Horizon evolution is mixed. Near-term and short-term expectations moved lower, and their uncertainty bands narrowed. Medium-term structure improved and remains in recovery from a negative state. Long-term structure softened and its uncertainty band widened. Current horizon relationships remain unresolved, and conditional confirmation across timeframes remains unclear because medium-term improvement is not supported by adjacent horizons.

Price behavior in this environment is shaped more by declining instability than by broad directional agreement. Compression in volatility supports calmer movement, but fragmented horizon structure keeps continuation quality uneven. The market state reflects lower surprise relative to prior expectations, not a fully coordinated positive or negative transition.

For decision context, this structure makes timing and signal reliability more important than directional conviction. Shorter-horizon strategies face a defensive near-term setup with limited directional evolution. Medium-term strategies face improving but incomplete structure. Longer-horizon views still have a constructive center, but the softening long-term state and wide uncertainty reduce confidence in persistence. The dominant risk is not only direction, but also whether movement remains reliable across timeframes.

Plainly, the market looks calmer but not fully resolved. Volatility is falling, the near-term view remains cautious, the medium-term view is improving, and the long-term view is still positive but weaker than before. The measured structure is useful as context, not as a trade instruction.

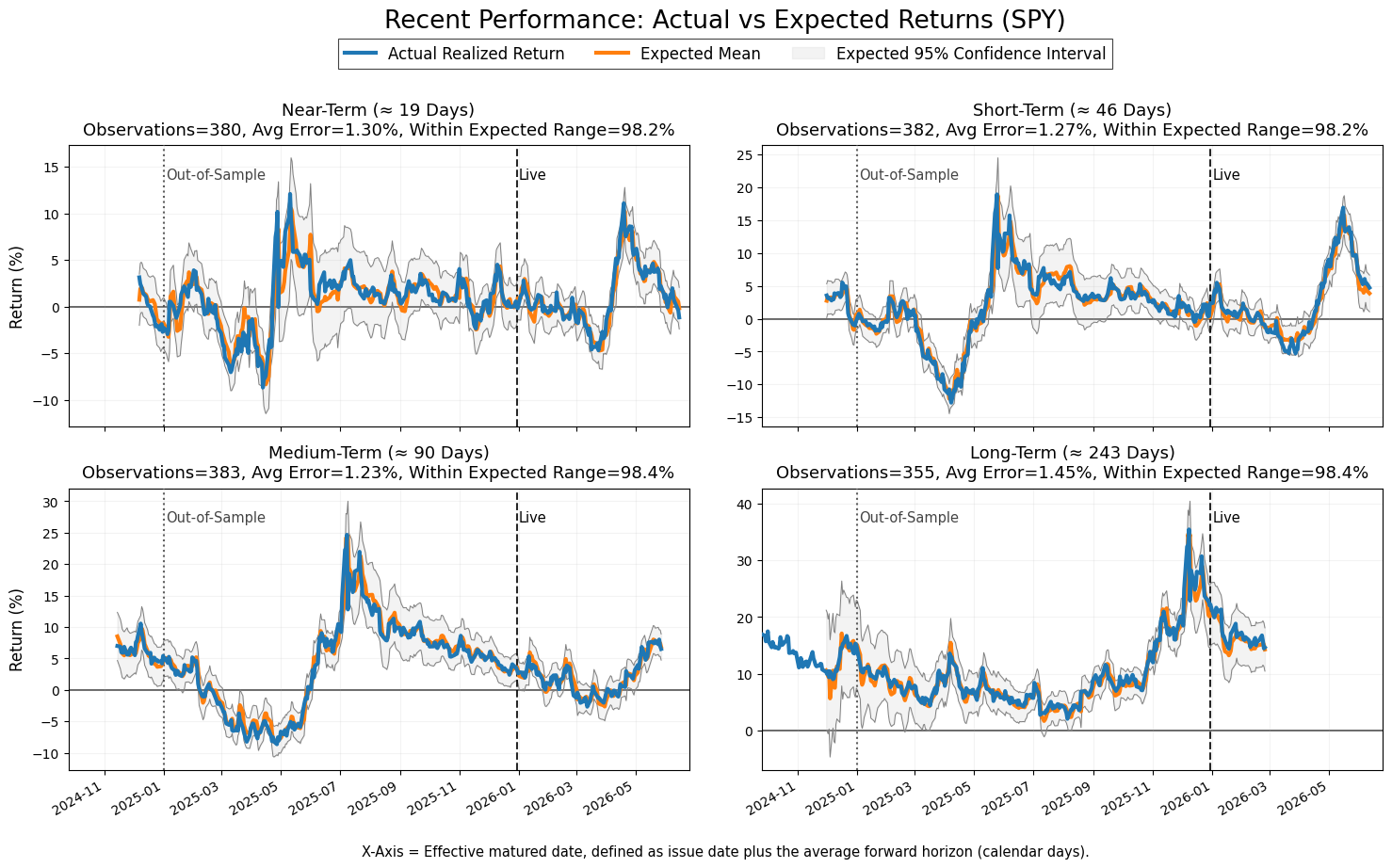

Model Calibration Assessment

This report is generated from the output of a proprietary quantitative system that measures current options market structure, conditions, and forward expectations. This section evaluates the correctness and calibration of the underlying model.

The model remains calibrated.

Across all four forecast horizons, realized returns continue to track the expected return estimates closely, with the large majority of realized outcomes remaining inside the projected 95% confidence intervals. Average forecast error remains stable across horizons, and confidence interval coverage continues to remain near the expected level. There is no visible evidence of systematic overestimation, underestimation, or persistent directional bias following either the out-of-sample or live deployment boundaries.

The innovation-based volatility signal also remains well aligned with realized market volatility. Periods of elevated model innovation continue to coincide with periods of elevated realized volatility, while declining innovation magnitude corresponds to calmer market conditions. The stability of this relationship through both the out-of-sample and live periods indicates that the model continues to adapt to changing market conditions without observable drift in its volatility measurement.

Overall, the validation diagnostics continue to indicate a stable, well-calibrated system. No material degradation, structural drift, or persistent bias is visible in either the return forecasts or the innovation-based volatility signal.

If you find this useful, you can support the work here. I’d also really appreciate hearing how you’re using this market data: any feedback helps me make this more useful in real workflows.

Trial API access to daily telemetry data is available upon request.