SPY Financial Telemetry – Apr 24, 2026

This report is generated from the output of a proprietary quantitative system that measures market structure, conditions, and forward expectations, translating system measurements into descriptive statements about the market environment.

Executive Summary

SPY remains in a compressing volatility regime where movement size and repricing speed are slowing, though residual instability from the prior higher-volatility environment remains present beneath the surface. Shorter horizons continue to exhibit reversal-driven and non-directional behavior, while longer-duration structure remains comparatively constructive. Cross-horizon alignment remains incomplete, leaving the broader environment transitional rather than fully stabilized.

Market Snapshot

Regime: Compressing volatility

Near-Term (~2–4 weeks): Non-directional, sensitive

Short-Term (~1–2 months): Transitional, resetting

Medium-Term (~2–4 months): Stabilizing, contained

Long-Term (~6–12 months): Constructive, moderate variability

Structure: Elevated, layered

Market State

- Volatility is compressing, which is associated with smaller and slower price movement, while the rising smoothed baseline reflects residual influence from the prior higher-volatility environment.

- Near-Term (~2–4 weeks) conditions are mixed with wide dispersion, which is associated with non-directional price behavior where reversals remain present despite reduced movement size.

- Short-Term (~1–2 months) conditions are mixed with moderate dispersion, which is associated with partial continuation that remains limited by repeated resets.

- Medium-Term (~2–4 months) conditions are mixed with tight dispersion, which is associated with more contained price movement where stabilization occurs without strong persistence.

- Long-Term (~6–12 months) conditions remain positive with moderate variability, which is associated with a constructive structure that continues to hold despite mixed shorter horizons.

- Cross-horizon behavior reflects disagreement, with longer-term structure remaining constructive while shorter horizons remain unresolved.

Implications

- Price movement reflects reduced magnitude, with smaller ranges following each repricing cycle.

- Short-horizon behavior reflects ongoing reversal patterns, with directional moves resolving without extension.

- Intermediate behavior reflects smoother transitions, with fewer abrupt shifts but limited continuation.

- Cross-horizon behavior reflects disagreement, with longer-term structure remaining constructive while shorter horizons remain unresolved.

What Changed This Week

- Near-Term (~2–4 weeks) expectations improved while dispersion expanded.

- Short-Term (~1–2 months) expectations improved while dispersion contracted.

- Medium-Term (~2–4 months) expectations weakened while dispersion contracted.

- Long-Term (~6–12 months) expectations strengthened while dispersion contracted.

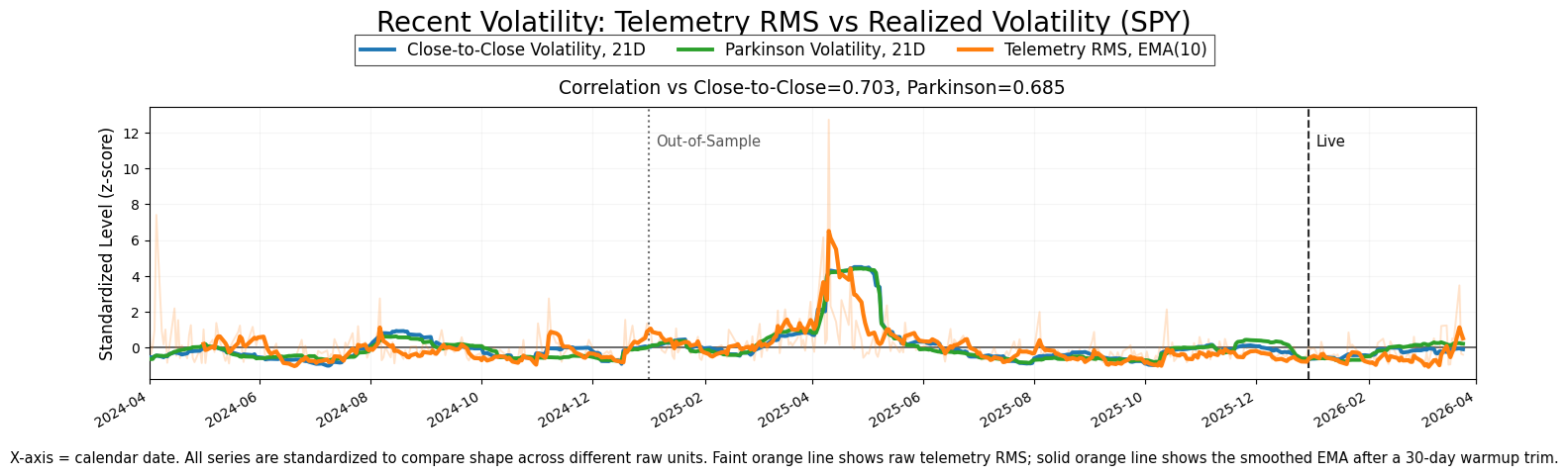

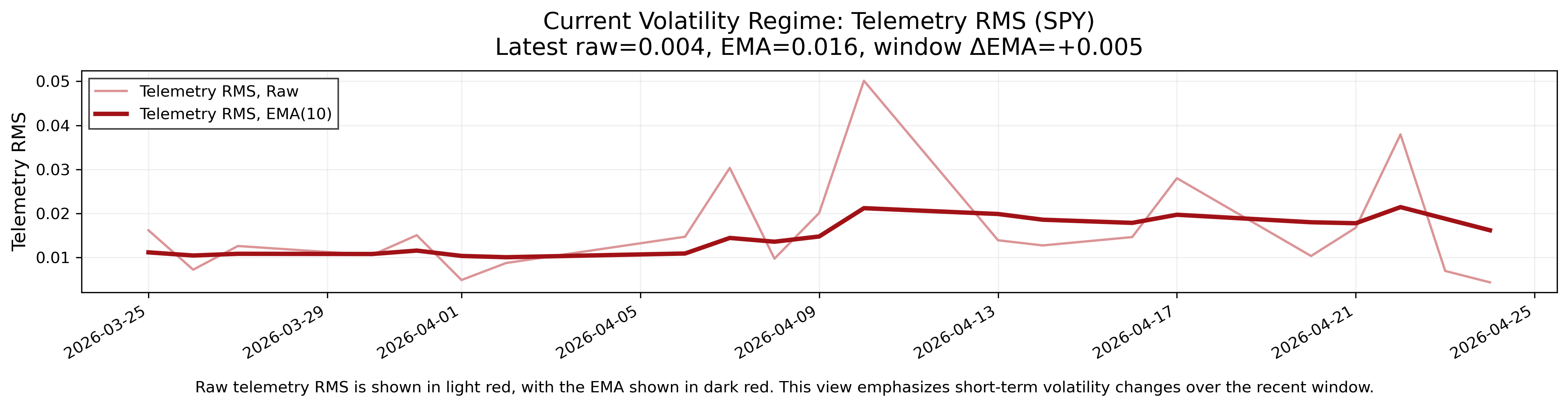

Volatility Regime

Volatility is compressing, as current movement is below the smoothed level, which is associated with reduced magnitude and slower price adjustment. At the same time, the smoothed level continues to rise, which reflects persistence from the prior regime. This combination is consistent with an environment where immediate price movement is more contained, while the broader system has not fully transitioned into a low-volatility steady state.

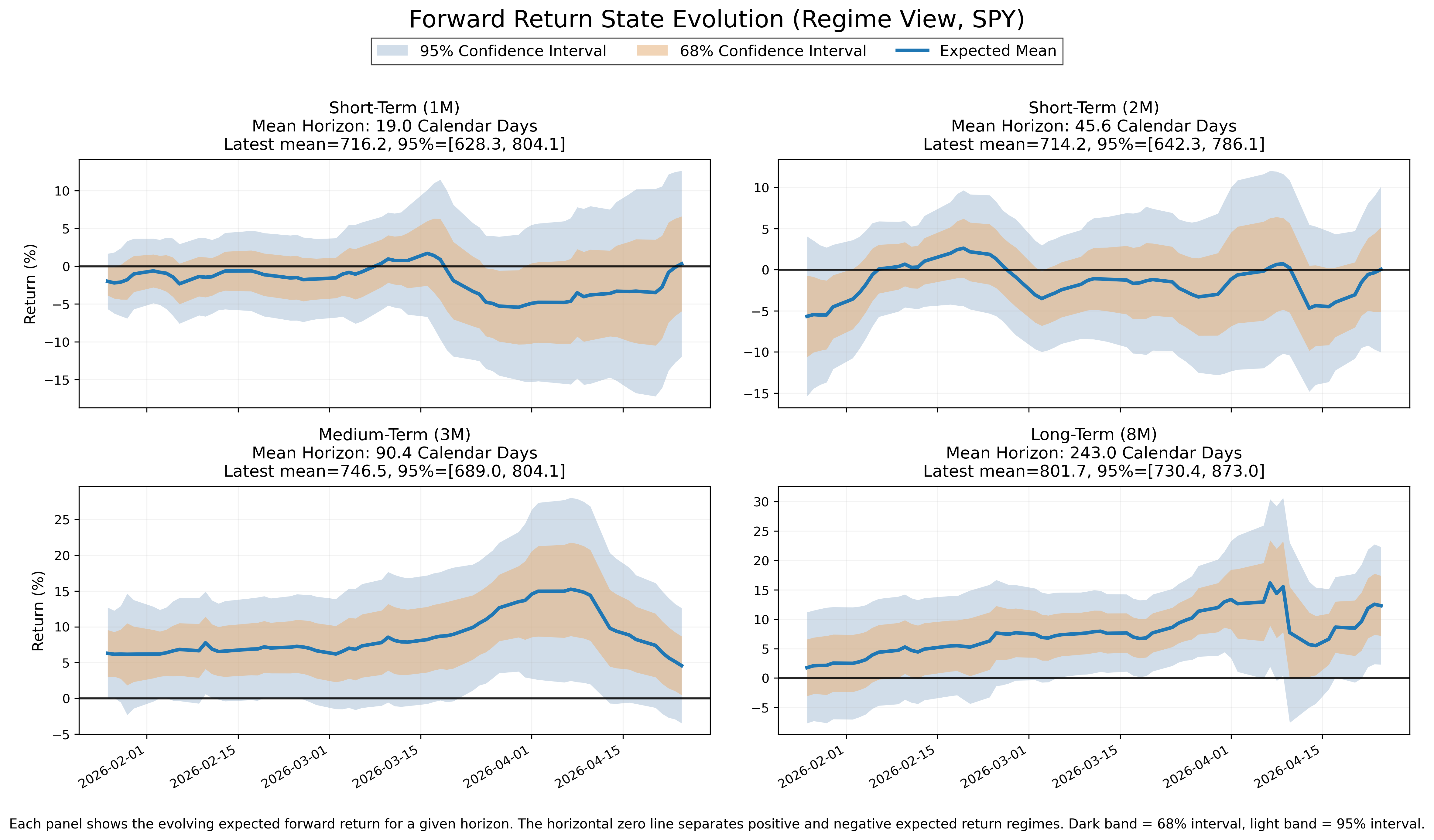

Forward Expectations

Near-Term (~2–4 weeks)

- State: Mixed

- Uncertainty: Wide

- Interpretation: Non-directional price behavior is associated with frequent reversals, while compressed volatility reduces the size of each move.

Short-Term (~1–2 months)

- State: Mixed

- Uncertainty: Moderate

- Interpretation: Transitional price behavior is associated with partial continuation, while resets limit sustained trend development.

Medium-Term (~2–4 months)

- State: Mixed

- Uncertainty: Tight

- Interpretation: Contained price behavior is associated with faster stabilization, while persistence remains limited.

Long-Term (~6–12 months)

- State: Positive

- Uncertainty: Moderate

- Interpretation: Constructive structure is associated with maintained directional bias, while variability remains within a moderate range.

This chart shows the evolution of expected forward return across time horizons. Each panel represents a different horizon, with the central line showing the expected mean and shaded regions showing uncertainty. This view reflects how market-implied expectations and dispersion have evolved over time.

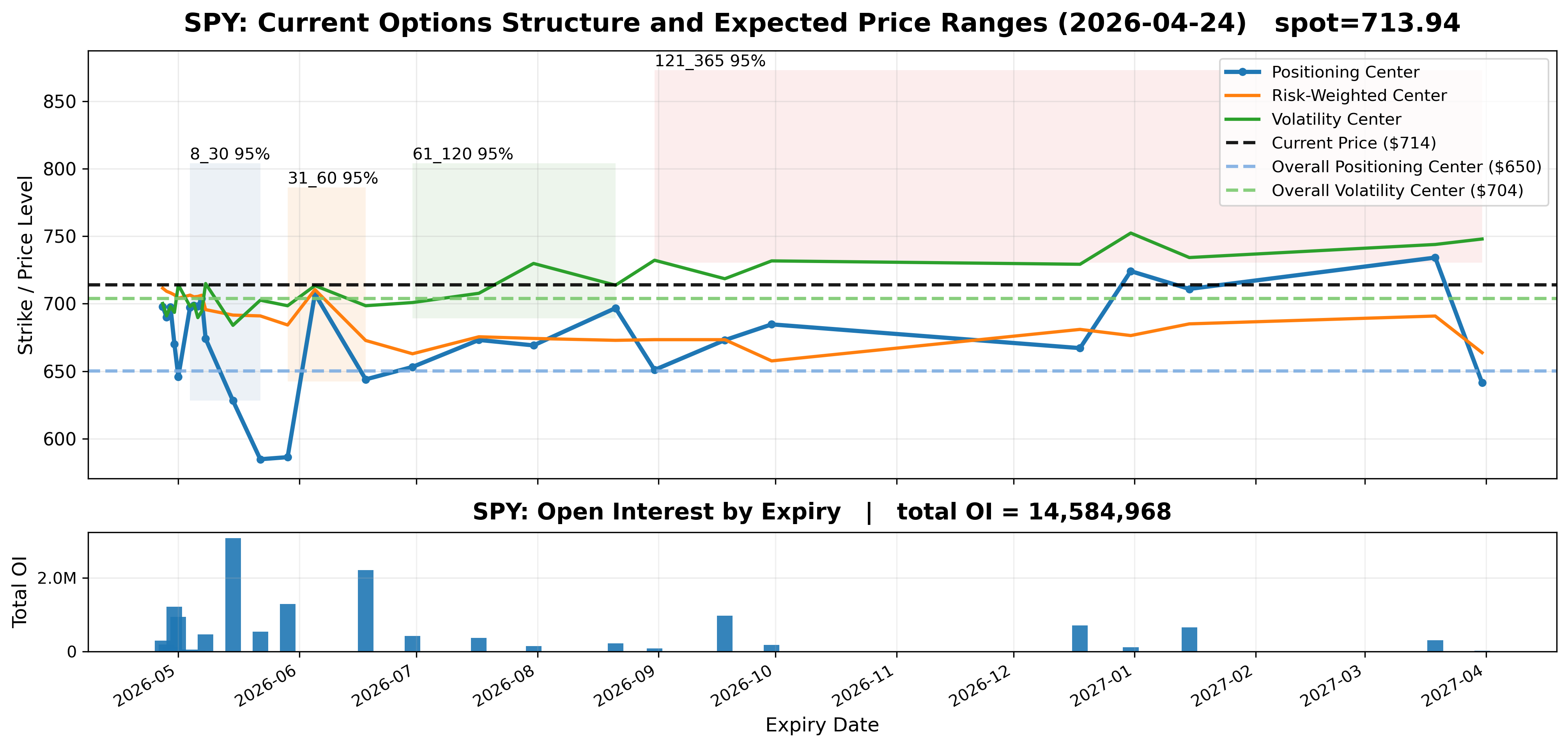

Current Market Structure (Context Only)

Price is positioned above aggregate positioning, risk-weighted, and volatility centers. Open interest is distributed across multiple expiries, with the largest concentration in the May 15, 2026 expiry. This reflects the current structure of positioning without implying directional outcomes or price impact.

Bottom Line

SPY is in a compressing volatility regime, where price behavior reflects smaller and slower movement. Short-term horizons remain non-directional with reversal-driven behavior, while longer-term structure remains constructive. Cross-horizon alignment remains incomplete, and the broader environment reflects transition rather than full stabilization.

Model Calibration Assessment

This report is generated from the output of a proprietary quantitative system that measures current market structure, conditions, and forward expectations. This section evaluates the correctness and calibration of the underlying model.

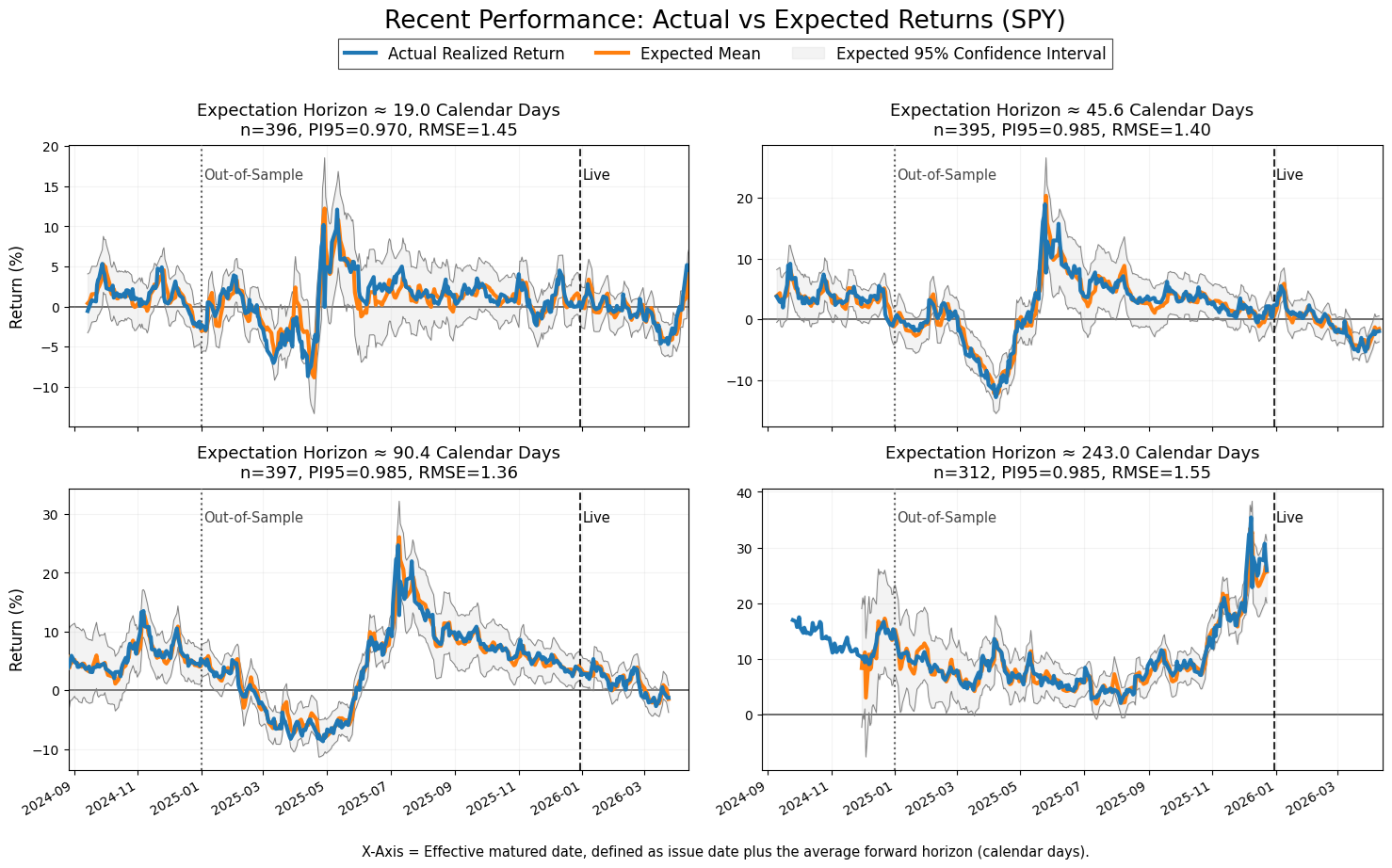

- Realized returns remain consistently contained within the expected 95% confidence intervals across all horizons. Interval breaches are infrequent and occur primarily during known volatility shocks, which is consistent with expected statistical behavior.

- Error distribution appears stable. Deviations between realized and expected values are symmetric and do not cluster persistently in one direction across time.

- There is no visible systematic bias. The expected mean tracks realized outcomes without sustained overprediction or underprediction.

- There is no observable drift. Model performance remains consistent across in-sample, out-of-sample, and live segments, with no degradation in alignment.

- Telemetry RMS maintains a stable relationship with realized volatility, with consistent co-movement and no structural breakdown in correlation.

Conclusion: Model remains calibrated.